Blog

Real Estate Offer Evaluation Checklist for Selling a Home

Posted by: CENTURY 21 Northwest

Date: March 20, 2018

CENTURY 21 Northwest Realty

Buy, Sell, Rent, Manage

Posted by: CENTURY 21 Northwest

Date: March 20, 2018

Whether you have outgrown it or are moving for other reasons, evaluating offers is one of the most exciting parts of selling a home. But with all of the variables (including emotions) that are tied up with being on the selling end of a real estate transaction, how can you be sure you are making a good decision? Luckily for you, we have put together this quick real estate offer evaluation to add to your selling a home checklist.

Once you’ve decided to put your home on the market, you wait expectantly for a potential buyer to make an offer. Everyone’s dream is to get multiple offers so they can pick and choose to find the best offer. (And a situation more and more are finding themselves in with the Phoenix-area real estate market currently favoring sellers.)

When you do get multiple offers, the challenge is an adequate analysis of any offer in light of your own needs and wants, not necessarily those of a potential buyer. Remember, the highest price offered may not be a part of an offer that is best for you. Even if you have only one offer for your property, a real estate offer evaluation of your property and purchase offer is important.

As the seller, you must always consider the net proceeds of an offer, not the asking price or any negotiated sales prices. The rule is: net proceeds count more than gross price. How much you, the seller, walk away with is what is important, along with time considerations. Using a selling a home checklist can help you evaluate multiple offers.

The expenses of selling a house are important. In addition to the real estate commission due the agents, there are other expenses that can have an impact on the net proceeds. The most common of these expenses is a seller requested concession. The best example of this is the buyer looking for concessions to help with the required down payment or asking the seller to subsidize closing costs on their behalf.

Compare these two offers, one with a seller concession and one without. Assume a starting price of $212,000. For the first offer, there is no concession, but buyer wants to pay a lower price of $207,500. In the second instance, the buyer is willing to start with the $212,000 asking price but wants a 4% seller concession which, in this case would be a concession of $8,480, resulting in $203,520. In this instance, the application of the seller concession means smaller net proceeds amount for the seller. Each offer has to be evaluated on its own.

Next is the appraisal. This is not a home inspection, but an opportunity for the lender to ensure that the house is in a safe condition and is worth the asking price. At this point, the lender can request that certain repairs be made before the sale, again reducing the net proceeds. Obviously, if the house is in good shape, there should be no impact as long the appraiser supports the asking price. Any repairs have to be factored into the net proceeds equation.

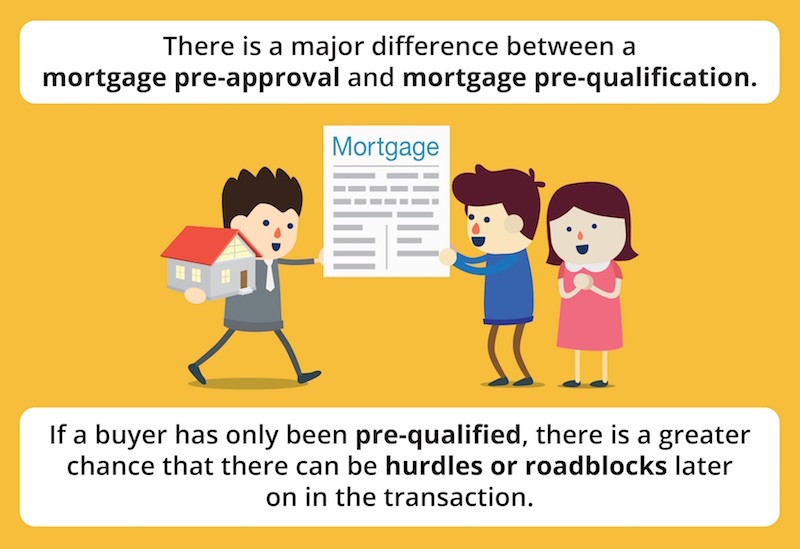

As a seller, you probably will not have detailed information about the buyer. You can easily get caught up in the process of real estate valuation. You won’t necessarily know a potential buyer’s income, financial situation, savings or credit score. The lender, however, is privy to that information. As the seller, you must know the difference between a buyer being pre-approved or pre-qualified. They are not the same thing.

A buyer that is pre-qualified has a lower standing than a buyer that is pre-approved. A pre-qualified buyer can still face hurdles along the way to the closing table. Most realtors know the reputation and standards of lenders in their area. They will know who the good, reliable lenders are and those do are lacking. This can be a make or break issue for a sales deal.

In addition, the type of mortgage the potential buyer is intending to use to finance the purchase of your property is important. FHA, VA or conventional mortgages all have different standards and requirements that can change over time. Credit scores and down payments play an important role in financing. Your real estate agent can help you determine what is real and what is simply a pipe dream in terms of buyer financing.

One final issue to be aware of is the dates and timing of financing commitments. Your real estate agent should be able to determine when the buyer can obtain a written formal mortgage commitment. This should take 2 – 3 weeks from application. If the process extends beyond that time, it’s time to question why it is taking so long.

The proposed closing date is important, especially to a seller who is most likely in the process of selling one residence and taking possession of another. Miscellaneous issues of contingencies can delay a closing or even cause a deal to fall through. Various inspections can eat up valuable time. These can include a home inspection, and inspections for mold, radon, structural, septic, chimney and pests.

You can offset this by having an inspection done on your own. It is not uncommon for a homeowner to have an inspection done just before putting their home on the market in order to discover and/or repair any defects. Another stumbling block is a buyer whose offer includes selling another property or getting out of a current lease. Your real estate agent can guide you on this and determine where the buyer is in that situation. The agent can usually determine the situation of a potential buyer. Is the property just on the market? Do they have an offer? Is this a stale listing or one that might simply be hard to sell?

Talk with your real estate agent to have a “bump clause” included in the offer. This right of refusal could be included in an offer, allow you to accept a fresh offer from a no contingency buyer.

Not everything on this selling a home checklist may apply to you. Remember, there’s a lot to consider in real estate offer evaluation. Work closely with your real estate agent to determine what is best for you, not necessarily the buyer.

Need help assessing offers on your home or want to get a real estate professional involved in the process before you reach that point? Give us a call today! Our realtors would be happy to chat with you and lend some advice for any stage of the selling process.